BMBI figures show timber Q1 value sales grow +0.9% year-on-year

BMBI figures show timber Q1 value sales grow +0.9% year-on-year

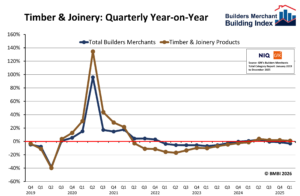

The latest figures from the Builders Merchants Building Index (BMBI) show Total Builders Merchants like-for-like value sales for Q1 2026, adjusted to remove the impact of trading days, were -3.2% lower than Q1 2025. Like-for-like volume sales were down -8.1%, with prices increasing +5.4%.

With no difference in trading days, unadjusted Q1 total value sales were also down -3.2% year-on-year. By value, seven categories sold more with Renewables and Water Saving (+14.3%) performing best. Of the two biggest categories, Timber and Joinery Products (+0.9%) performed better than Total Builders Merchants, but Heavy Building Materials fell -6.7%.

March 2026 like-for-like value sales were -3.6% lower than March 2025. Like-for-like volume sales dropped -7.8% while prices increased +4.6%. With one additional trading day in March 2026, unadjusted total value sales were up +1.0% year-on-year. Unadjusted volumes were down -3.4% and prices were up +4.6%.

Ten categories sold more by unadjusted value, with Renewables & Water Saving (+14.5%) the standout category. Timber & Joinery Products (+4.2%) outperformed Total Builders Merchants.

James Davenport, Managing Director of Metsä Wood UK and BMBI’s Expert for Softwoods and Engineered Timber said: “The UK market for both softwoods and engineered wood products has been subdued in Q1 2026.

“Merchant and distributor restocking in January generated volumes broadly in line with January 2025. However, follow-up demand was slower than expected, reflecting a cautious approach to stockholding.

“Wet weather in February across the majority of England and Wales certainly weakened demand from the housebuilding sector and impacted the stock build of timber landscaping products in preparation for the outdoor season.

“March brought further uncertainty with the conflict in Iran, and wider geopolitical and economic pressures compounding existing challenges around fuel, energy, borrowing costs, and consumer confidence.

“These factors are shaping activity in the housebuilding sector, prompting the Construction Products Association (CPA) to revise down its 2026 outlook. Its latest Spring forecast suggests a difficult year for construction, including a forecast decline in private housing output.

“Project costs across both RMI (Repair Maintenance & Improvement) and construction remain under pressure, and this will likely further weaken demand over the coming months.”

For the latest reports, Expert comments and Round Table Debates, visit www.bmbi.co.uk.

More news

Taking on an apprentice: Costs, wages and support

MRA Analyst on construction data and conservation